Why “Clean Books” Don’t Always Mean Low CRA Risk

Many Ontario corporations file a technically correct T2 and still get a CRA “matching” letter or review request. That’s because CRA doesn’t only assess your T2 in isolation—it cross-checks your filing against other data sources.

The result: small inconsistencies between your books, slips, payroll, HST, bank activity, and prior-year filings can trigger follow-up. These aren’t always “mistakes”—but they often require time-consuming reconciliation and supporting documents.

What CRA Often Cross-Checks Against Your T2

- T4 payroll filings and remittances

- T5/T4A slips (where applicable)

- HST returns (for registrants)

- Corporate bank activity and year-end cutoffs

- Prior-year comparatives (swings in revenue/expenses/loans)

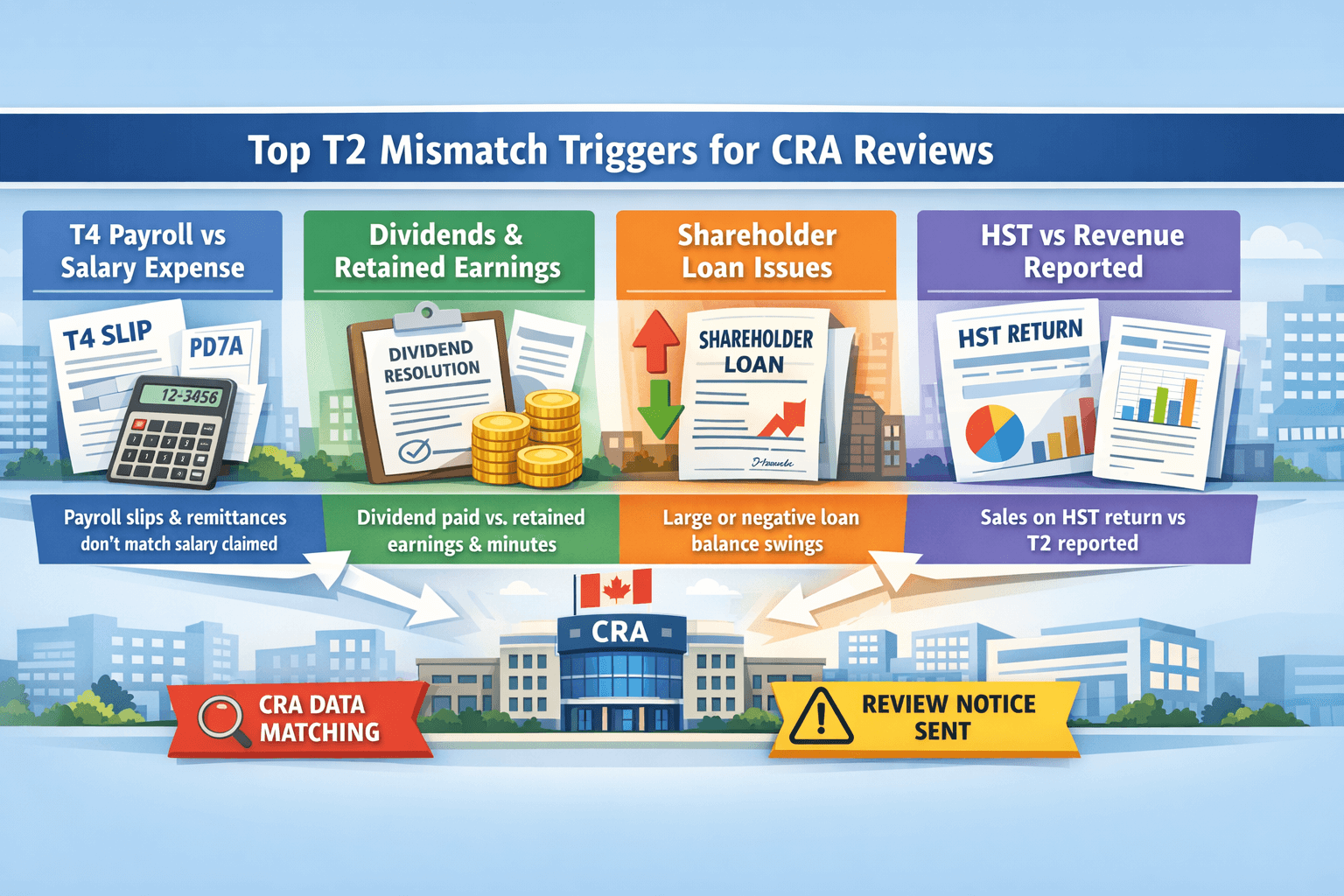

The Most Common T2 Mismatches That Trigger CRA Reviews

1) Salary expense vs T4/PD7A totals

A classic trigger: the corporation deducts salary on the T2 (or books), but the T4 slips and payroll reporting don’t reconcile cleanly. Even minor differences can cause CRA to ask for a reconciliation.

Common causes include year-end adjustments not reflected in payroll, last-minute bonuses, or bookkeeping/payroll handled in separate systems. (Related reading: Salary vs Dividends in Ontario.)

2) Dividends paid vs retained earnings and documentation

Dividend planning can be efficient—but it must be supported properly. CRA can request evidence of: director/shareholder resolutions, minutes, and that the corporation had sufficient retained earnings.

3) Shareholder loan fluctuations (due to/from shareholder)

Large swings, negative balances, or unusual year-end timing can prompt questions. The issue is often not the balance itself—it’s whether the story is consistent across your records and filings.

4) HST revenue vs financial statement/T2 revenue

CRA often compares revenue reported on HST returns versus revenue in your financial statements and T2. Timing differences can be valid, but unexplained mismatches can trigger follow-up.

A Practical Pre-Filing Alignment Checklist

Before filing your T2, it’s worth doing a quick alignment check:

- Reconcile salary expense to T4 reporting and payroll remittances

- Ensure dividends are documented (minutes/resolutions) and supported by retained earnings

- Review shareholder loan movements for consistency and clear explanations

- Compare HST revenue vs accounting revenue and document timing differences

- Confirm that year-end financial statements and the T2 tell the same story

What This Means for Your Next Corporate Year-End

If your goal is simply to file quickly, you may still spend time later responding to CRA. If your goal is to file cleanly and defensibly, you want payroll, slips, HST, books, and T2 aligned before submission.

FAQ

Is getting a CRA review letter the same as an audit?

Not necessarily. Many corporate review letters are targeted “matching” requests for support and reconciliation. Still, they can take time and should be handled carefully.

Do I need to worry if my HST revenue doesn’t match my accounting revenue exactly?

Differences can be normal due to timing and reporting methods. The key is being able to explain and document the reason for any variance.

What’s the easiest way to reduce mismatch risk?

Align year-end financial statements, payroll/slips, and the T2 as one integrated process—rather than separate “tasks” done by different people.