7 CRA Red Flags That Trigger Corporate Tax Audits (And How to Avoid Them)

Corporate tax audits don’t happen randomly. In most cases, the CRA flags

specific patterns on T2 corporate tax returns that indicate higher risk.

If you own an incorporated business in Ontario, understanding these red flags

can significantly reduce your audit exposure.

At Podolsky Accounting, we regularly assist corporations facing CRA reviews

and audits — and the same issues appear repeatedly.

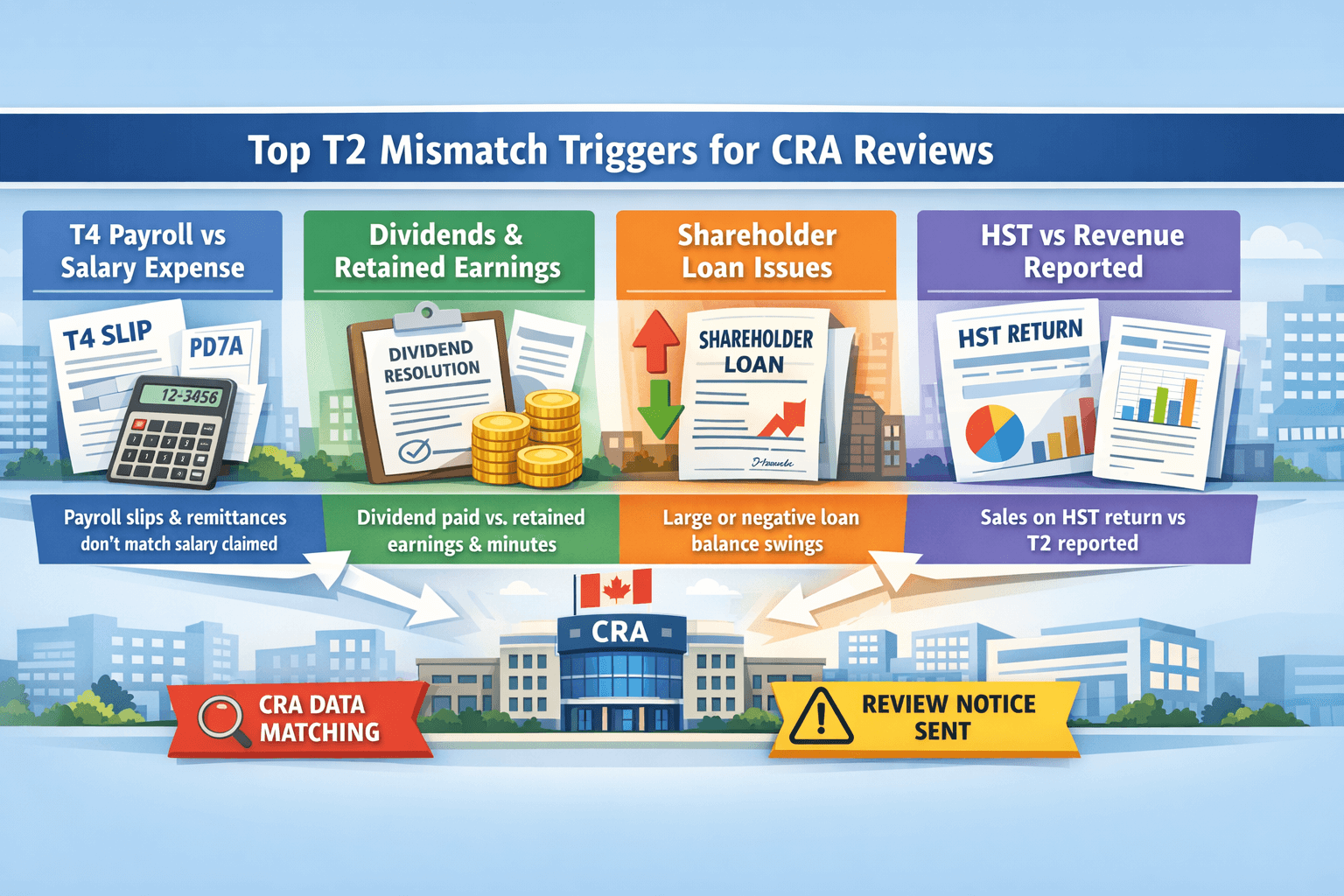

1. Shareholder Loan Accounts That Don’t Make Sense

One of the most common CRA audit triggers is an improperly reported

shareholder loan balance. Overdrawn or uncleared shareholder loans can

quickly lead to reassessments and taxable benefits.

CRA often focuses on:

- Large year-end shareholder loan balances

- Loans not repaid within the required time frame

- Missing documentation or inconsistent reporting

2. High Expenses Relative to Revenue

Corporations reporting unusually high expenses compared to revenue

frequently trigger CRA reviews. This is especially common in

owner-managed small businesses.

CRA pays close attention to:

- Vehicle and home office expenses

- Meals and entertainment

- Personal expenses run through the corporation

3. Inconsistent HST and T2 Reporting

If your HST filings don’t align with your T2 corporate tax return,

the CRA’s systems will notice. HST mismatches are one of the fastest

ways to trigger a desk audit.

This often happens when bookkeeping and tax filing are handled separately

without professional review.

4. Repeated Losses Year After Year

Corporations that report losses consistently may be flagged to determine

whether the business is truly commercial or partially personal in nature.

CRA may question:

- Business intent and profitability

- Expense deductibility

- Whether the corporation is being used for tax deferral only

5. Late or Missing T2 Filings

Even inactive corporations must file a T2 return. Repeated late filings

or missing returns significantly increase audit and penalty risk.

Professional

corporate tax return services

help prevent these issues entirely.

6. Aggressive Salary vs Dividend Splits

Improper compensation planning can raise CRA concerns, especially when

dividends or salaries fluctuate without clear reasoning.

A CPA ensures compensation strategies are tax-efficient and defensible.

7. DIY Corporate Tax Filings

Self-prepared T2 returns often contain technical errors that trigger CRA

follow-up. Unlike personal returns, corporate filings involve complex

schedules that CRA reviews carefully.

If you’re unsure whether professional help is necessary, read:

Do I Need an Accountant for My Small Business?

How a CPA Reduces CRA Audit Risk

At Podolsky Accounting, we don’t just file T2 returns — we prepare them

with audit defense in mind. Our approach includes:

- CRA-compliant reporting positions

- Clean, supportable financial statements

- Proper documentation and disclosures

- CRA audit and review support if needed

We also provide

audit and assurance services

for corporations requiring higher-level reporting.

Concerned About CRA Audit Risk?

If your corporation is filing a T2 or has received CRA correspondence,

working with an experienced CPA can make all the difference.

📞 Call 416-856-8897 or

request a consultation online.

If you want these issues reviewed before CRA does, our

corporate tax return services in Ontario

help small business owners and corporations file accurate T2 returns with confidence.